July 2023 - Monthly Market Monitor

July 2023 - Monthly Market Monitor

In the month of July…

The Russell 3000, an index designed to capture the total domestic stock market, gained +3.6%, bringing its year-to-date gain to +20.3%

Cap Size = July, YTD Return

Large Core = +3.4%, +20.7%

Mid Core = +4.0%, +13.3%

Small Core = +6.1%, +14.7%

Value-style indices outperformed their growth counterparts across all capitalization styles. Income (dividends) was a strong driver in the month, in a reversal of what we have seen in the year thus far. The Dow Jones U.S Select Dividend Index gained 4.2% in July, bringing its year-to-date return to -0.3%

Cap Size = Growth, Value Monthly Return

Large = +3.4%, +3.5%

Mid = +3.0%, +4.4%

Small = +4.7%, +7.6%

Sector performances were positive across the board. The returns shown are for large cap.

Sector = July, YTD Return

Communication Services = +6.9%, +45.7%

Consumer Discretionary = +2.4%, +36.3%

Consumer Staples = +2.1%, +3.5%

Energy = +7.4%, +1.5%

Financials = +4.9%, +4.3%

Health Care = +1.0%, -0.5%

Industrials = +2.9%, +13.4%

Information Technology = +2.7%, +45.7%

Materials = +11.4%, +11.4%

Real Estate = +1.3%, +5.1%

Utilities = +2.5%, -3.4%

International equities gained +3.3%. Every country, besides Portugal (-0.1%), saw gains. All regions saw similar gains. The “worst” region was the Nordic countries which saw an overall gain of 1.7%. The best perforimg region was the Pacific ex. Japan which saw gains of 4.4%.

Emerging market equities gained +6.9%. All regions were positive. China bounced back this month, especially the larger names. Chinese equites were up +10.9%, with the largest 50 up +12.5%.

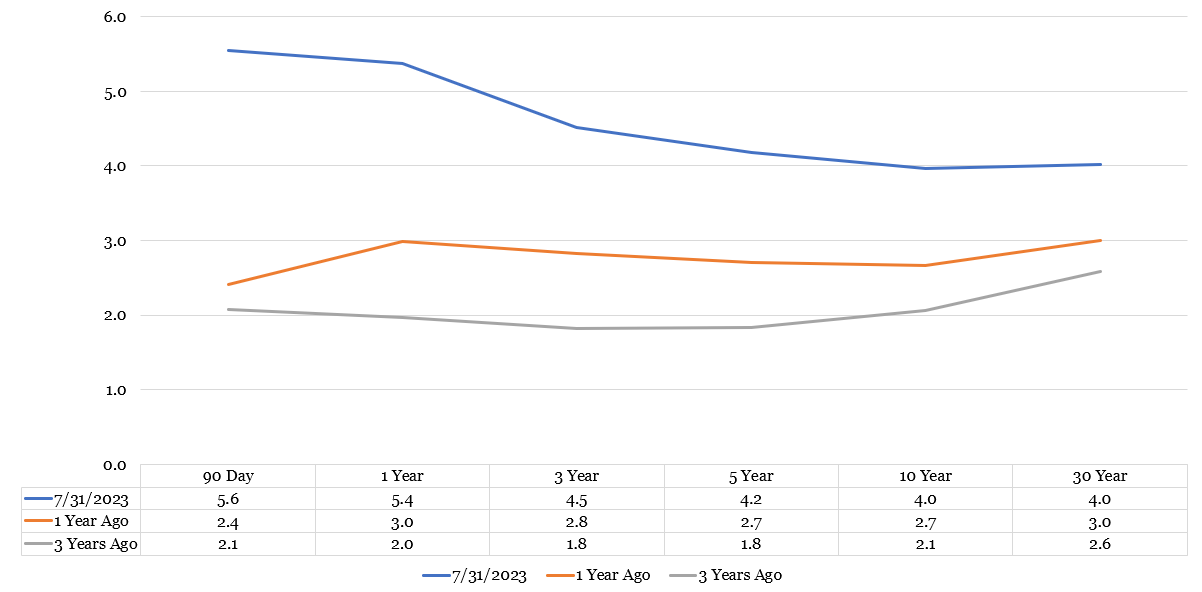

Fixed income markets were mixed. The yield curve stayed relatively flat, though the front-end and long-end of the treasury curve moved up a touch (90 Day = 5.3% → 5.5% & 30-Year 3.9% → 4.1%). Spread instruments (high yield and general corporates) outperformed treasuries and longer-duration outperformed shorter duration.

The S&P GSCI Index (a market proxy for commodities) gained +6.7%. They are now relatively flat year-to-date +0.6%. Here are the returns of the underlying components:

Sub-sector = July Return, YTD

Agriculture = +3.0%, -0.5%

Energy = +16.0%, +2.6%

Industrial Metals = +6.5%, -2.5%

Precious Metals = +3.2%, +7.7%

Livestock = +2.0%, +10.40%

Economics

Consumer spending increased by 0.5%, with gains across both goods and services. It was expected to rise by 0.4%.

However, personal income increased by less than expected (0.3% vs. 0.5%)

The personal savings rate is down to 4.3%.

Household debt service payments as a percentage of disposal personal income is approximately back to levels seen in 2019 (9.6%). However, this is still well below the highs of 2007 (13.2%).

The Federal Reserve hiked interest rates by 0.25%, bringing the Fed Funds rate range to 5.25%-5.50%.

While it seems likely that the Federal Reserve will “pause”, they have in no way ruled out future hikes.

Inflation has continued to come down but is likely to be range-bound for a good period of time (3-9 months). So, while we would not be surprised to see inflation come down a bit from here, we think it’s just as likely to move up slightly given seasonal dynamics in energy as well as recent developments in the real estate market.

The Federal Reserve Bank of Cleveland is forecasting year-over-year CPI of 3.37%, and Core CPI of 4.91% at the end of the month.

Truflation, which we believe is an imperfect but useful forward indicator, has current year-over-year inflation at 2.25%.

Wage gains seen over the last year have moderated. The last survey saw wages growing 1.0%, relative to the surveyed results of 1.1%.

Retail inventories keep rising more than expected, which should continue to provide pressure to both pricing and margins. The actual growth in inventories was 0.7%, relative to the survey of 0.4%. However, these results are typically done in nominal not real (inflation-adjusted) terms. Inventories are now at about the same levels as in 2019.

Both imports and exports of goods to and from the United States have decreased year to date.

Imports have declined faster than exports, which has decreased our net deficit by ~10B.

30-year fixed mortgage rates are holding steady at about 7%, though they have not been nearly as effective in holding back demand as initially anticipated. Demand is still noticeably outpacing supply.

The yield curve remains inverted. The curve has moved dramatically over the last three years. The 1.4% differential compounded over 30 years is substantial. Now do this math for total paid to mortgages!

4.0% over 30 years = 224%

2.6% over 30 years = 116%

What’s Interesting this Month?

Wall Street Journal

“Biotech Stocks Join AI-Fueled Rally”

In the world of healthcare stocks, this year has been a rollercoaster ride. However, amidst the struggles, a few small players are defying the odds with the help of artificial intelligence (AI). While the S&P 500's healthcare sector lags behind, tech companies like Nvidia and Microsoft are soaring high due to the AI revolution. This enthusiasm has given a boost to smaller biotech firms implementing AI in drug discovery and diagnostics. Investors are placing bets on the potential growth of these AI-focused companies, despite their current lack of consistent profits. The promise of AI disrupting the healthcare industry presents exciting possibilities for investors and patients alike. As Justin Simon, portfolio manager at Jasper Capital Management says:

The reality is 18%-20% of GDP is in healthcare, and if you make a difference there, there’s plenty of market opportunity.

www.wsj.com/biotech-stocks-join-ai-fueled-rally

------------------------------------------

Bloomberg

“Americans Prepare for Tighter Budgets as Student Loan Payments Resume”

With the most recent ruling by the Supreme Court striking down Biden’s student loan forgiveness, millions of Americans are now reconsidering their finances going forward. As the assumption of forgiveness is now gone, and the loan payments are set to resume in October, borrowers will have to adjust spending elsewhere to make up the slack. While consumer spending has remained relatively stout despite many fearing a recession, the average of about $400 in monthly student loan payments is certain to affect at least the 27 million borrowers.

www.bloomberg.com/student-loan-payments-resuming-likely-to-dampen-spending

------------------------------------------

Axios

“The stock market’s up big this year — but not because of earnings growth”

The phrase of the year should be multiple expansion.

https://www.axios.com/us-stocks-earnings-growth-2023

------------------------------------------

Bloomberg

“Lots of US Homeowners Want to Move. They Just Have Nowhere to Go”

Locked into cheaper borrowing costs and unable to find a new place that fits their budgets, countless people are opting to remain in their current homes, adding to an acute shortage of available properties.

bloomberg.com/housing-market-is-stuck-as-homeowners-stay-put

------------------------------------------

Harvard Business Review

“The Key to Great Strategies? Timing”

History is littered with examples of ideas that came before their time. And many strategies have misfired when they weren't quite ready to capture the moment in which they might have thrived. What's great about this podcast (or transcript) is it examines the importance of timing when it comes to strategies for organizations ... and how we strategize about tasks and goals in our individual lives.

https://hbr.org/the-key-to-great-strategies-timing

------------------------------------------

Visual Capitalist

www.visualcapitalist.com/the-top-performing-sp-500-sectors-over-the-business-cycle/

------------------------------------------

The Atlantic

“America Is Drowning in Packages”

In 2000, the United States Postal Service—the country’s biggest parcel shipper—delivered 2.4 billion packages. By 2022, that number had ballooned to 7.2 billion. Our population has not grown 3 times in those years. The impact of the massive spike in package deliveries spans from more trucks on the road, to more semis on the interstate and large delivery vehicles on residential streets, to more stress on asphalt and bridges, to more accidents and injuries… etc. Furthermore, despite the rise in package count, the jump in delivery workers has not been one-to-one, and the cracks are clearly showing.

www.theatlantic.com/ups-strike-union-contract-package-deliveries/

------------------------------------------

Modern Farmer

“The World Could Lose Half of all Farms by 2100”

A lively study from the University of Colorado, Boulder reveals a future where farms worldwide undergo a significant shrinkage, leading to potential challenges in our food system. Published in Nature Sustainability, the study used a model to predict the evolution of farms up to 2100, showing a drop in farm numbers to 272 million from 616 million in 2020. As economies grow stronger, more people abandon rural areas for urban living, reducing the number of farmers and increasing the size of farms. This consolidation may result in fewer diverse farms, posing risks to our food supply and necessitating support for future farmers.

https://modernfarmer.com/2023/07/the-world-could-lose-half-of-all-farms-by-2100/

------------------------------------------